Turkish Central Bank Sends Gold To London. In Need for FX?

Written by Jan Nieuwenhuijs, originally published at Gainesville Coins.

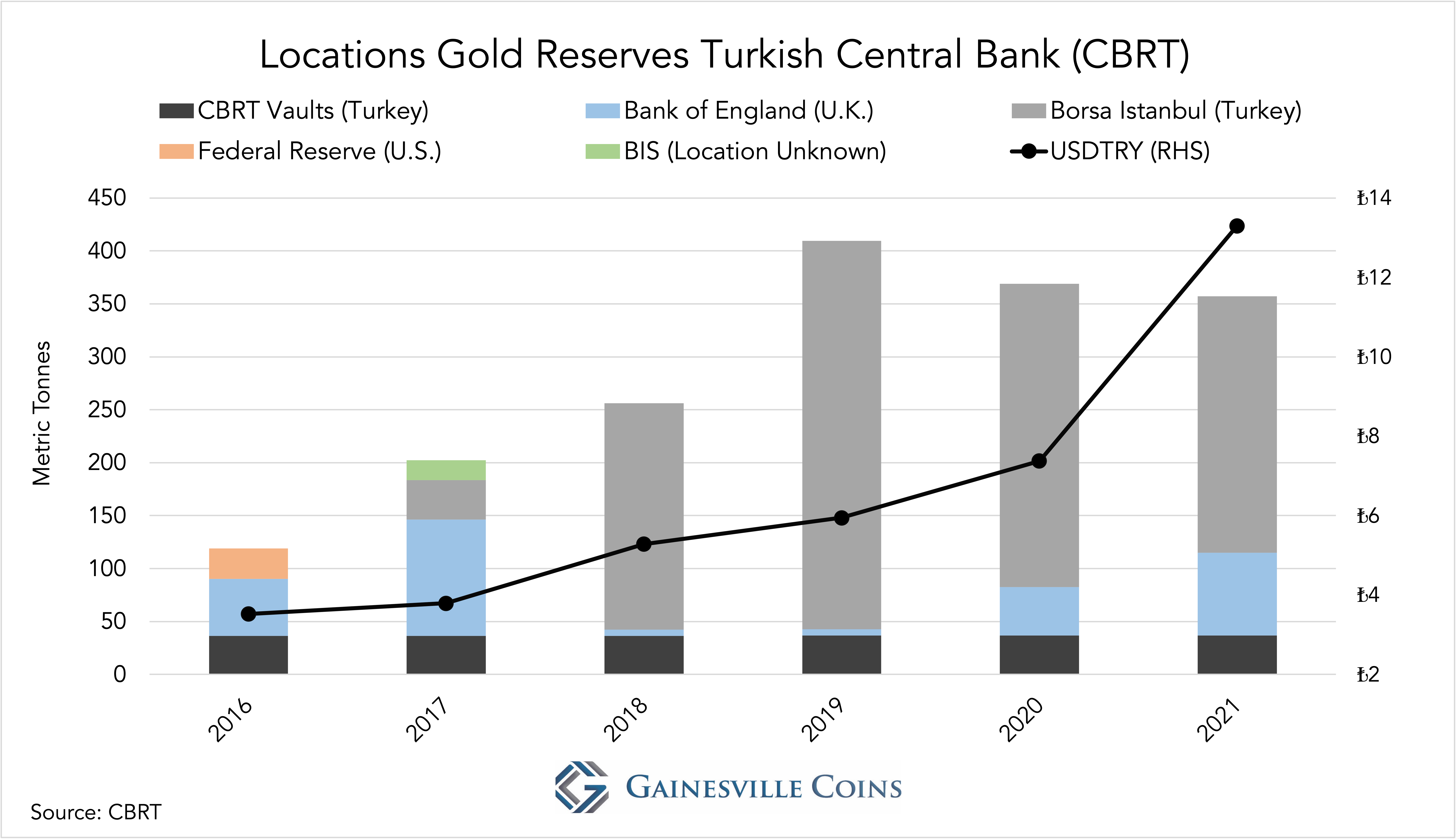

After having repatriated 104 tonnes from the Bank of England (BOE) in 2018, the Central Bank of Turkey (CBRT) has been sending gold back to London in 2020 and 2021. Amid economic turmoil that’s weakening the Turkish lira, CBRT is likely using its gold at BOE as collateral for foreign exchange (FX) loans. Turkey’s situation is reminiscent of Venezuela several years ago.

Computing Turkey’s net gold reserves is complicated, because since 2011 CBRT and the Turkish Treasury have launched several schemes to borrow gold, which all show up on the central bank’s balance sheet. Simplified, what I have done is take the tonnage “owned by the central bank” in CBRT’s annual report—this excludes gold submitted by banks for reserve requirements and the Treasury’s gold—and subtracted outstanding Turkish lira for gold swaps*.

The World Gold Council (WGC) computes Turkish net gold reserves differently. My estimate for Turkey’s net gold reserves on December 31, 2021, is 354 tonnes, roughly 300 tonnes less than what the IMF reports, while the WGC discloses 394 tonnes. A more detailed discussion on this topic can be found in the Appendix.

*A swap in this article refers to a spot sale (for example, selling gold for dollars) that is unwound by a forward transaction (buying gold with dollars) for a slightly higher price reflecting an interest rate. A swap can also be viewed as a collateralized loan (borrowing dollars with gold as collateral).

Sending Back Repatriated Gold

In 2017 and 2018 CBRT repatriated all its gold from the Federal Reserve Bank of New York (FRBNY) and the Bank for International Settlements (BIS), and all but 6 tonnes from BOE, according to its annual reports. All the repatriated gold was moved into the vaults of Borsa Istanbul. CBRT is highly influenced by Turkish President Erdogan, who has strained ties with the West. The central bank prefers to store gold on its own soil, preventing rivals from having leverage in disputes.

Yet in 2020 CBRT began shipping gold back from Turkey to London, which is one of the most liquid gold markets globally. At the end of 2021 CBRT was holding 78 tonnes at the BOE. Possibly, it wants to hold gold in London for an emergency sale. More likely the gold is being swapped for FX to defend the lira or make international payments.

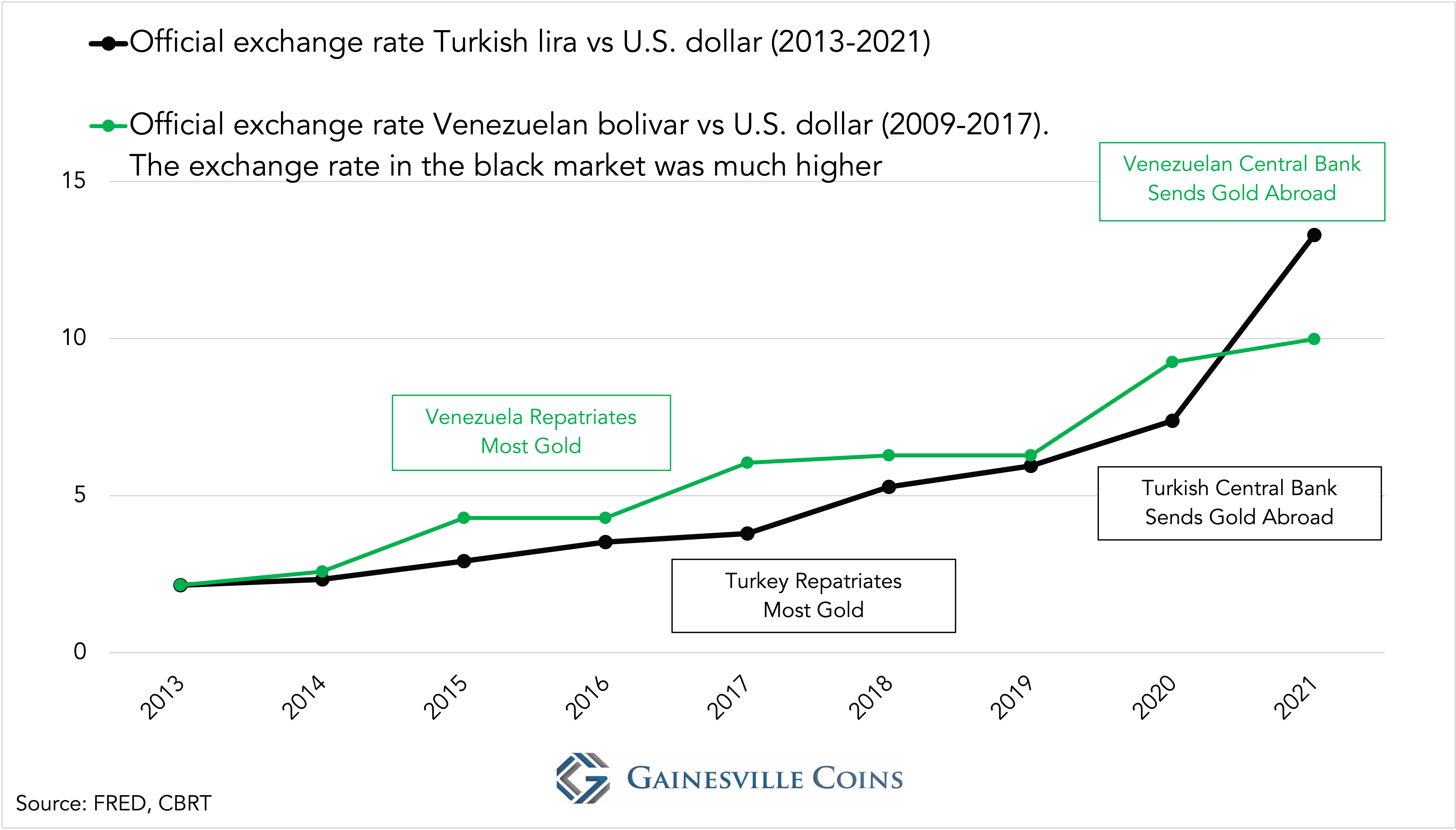

Turkey’s economy is in dire straits. Consumer price inflation is at 80% and the Turkish lira has lost 90% of its value versus the U.S. dollar in less than 14 years. The currency crisis is eating into Turkey’s FX reserves.

Parallels With Venezuela

The similarities between Turkey and Venezuela are striking, first and foremost because both countries’ economic policy is irrational. In 2011, socialist Hugo Chavez, then President of Venezuela, ordered 85% of the central bank’s gold reserves to be repatriated in an act of economic nationalism. Two years later, due to ruinous monetary policy, inflation reached 40% and the Venezuelan bolivar began its steep descent. In need for FX the Venezuelan central bank (BCV) signed a swap agreement, using its gold that was still in London, with Citibank in 2015. “The value of the gold will continue to appear on the Central Bank’s balance sheet,” it was reported at the time.

In 2016, I reported that BCV was shipping its gold to Switzerland in need for more FX. Financial conditions didn’t improve in Venezuela led by socialists, and in 2017 BCV allowed a swap to lapse. The gold collateral was lost. By then Venezuela had already reached hyperinflation.

In the following years Venezuela continued to sell monetary gold abroad to pay for the imports of basic goods. In addition, current President Maduro makes money off smuggling conflict gold. How much monetary gold BCV has left is any one’s guess.

In turn, President Erdogan doesn’t believe in raising interest rates to stop the lira from plummeting in value. He thinks higher interest rates will fuel inflation, instead of the other way around. On the first of January of this year, it took 13 Turkish liras to buy 1 U.S. dollar; at the time of writing, it takes 18 liras. This will not end well if Erdogan continues to control CBRT and assumes inflation will magically disappear by itself.

Conclusion

There is intense pressure on CBRT’s international reserves—gold, FX, and SDRs. My estimate for CBRT’s net gold holdings is at most 354 tonnes (end 2021) but can be significantly lower if some of it has been swapped for FX in London. In case all CBRT’s gold at BOE is on swap, 78 tonnes must be deducted from the total (354 – 78 = 276). When Turkey can’t unwind the swap by buying back their gold, the collateral is lost.

I didn’t manage to find off balance sheet data that reveals how much gold CRBT has swapped out. I did find a quote in an LBMA special on the Turkish gold market published in August 2021. From the LBMA:

After Turkish foreign exchange reserves dropped to a multi-decade low over the summer, some gold holdings are believed to have been mobilized to support the lira and/or repay international debt.

It could be this quote refers to gold for FX swaps by CBRT in London.

According to this website by two Turkish economists, CBRT’s net international reserves were negative in 2021, when taking into account all (on and off balance sheet) FX liabilities. More recently Reuters reported Turkey’s net international reserves are negative. If true—I haven’t been able to calculate CBRT’s net FX reserves myself—this means that Turkey won’t be able to pay its international debt obligations, even it sells all its gold and SDRs. Only an emergency loan by the IMF or a miracle can save it.

Appendix

The following explains how I have computed Turkey’s net gold reserves.

Starting in 2011, CBRT allowed commercial banks to fulfill their lira reserve requirements partly in gold. The aim was to attract physical gold from “under-the-mattress” into the financial system, which banks would use for reserve requirements (RR), freeing up lira liquidity. Gold QE, if you will. The scheme was modestly successful, because most of the gold submitted for RR by banks was borrowed in London. This facility is called the Reserve Option Mechanism (ROM).

In 2018, the Turkish Treasury began issuing gold bonds. The gold borrowed is transferred to CBRT’s balance sheet, and thus increases CBRT’s gross gold reserves and gold liabilities to the Treasury. Issuing of gold bonds has intensified, as measured by CBRT’s gold liabilities to the Treasury. See the chart below.

In 2019, CBRT set up a lira for gold swap market. Turkish commercial banks can swap gold for liras at their central bank, which incentivizes banks to attract physical gold from investors. CBRT simply prints liras to pay for the swaps. Off balance sheet swap data by CBRT published here allowed me to compute the total amount of gold swaps outstanding (buy side, quotation and auction method).

As mentioned earlier, my starting point in calculating CBRT’s net gold reserves has been the tonnage “owned by the central bank” in the annual reports. Cross checks confirm this amount excludes gold in the ROM facility and the Treasury’s gold on CBRT balance sheet. Subsequently, I have subtracted the total amount of gold swaps outstanding from the total. The result is my estimate for Turkey’s net gold reserves.

For those interested, here is a paper by the World Gold Council on how they measure Turkey’s net gold reserves.

Thanks for the article!

(The link for the off balance sheet swap data by CBRT is not working)